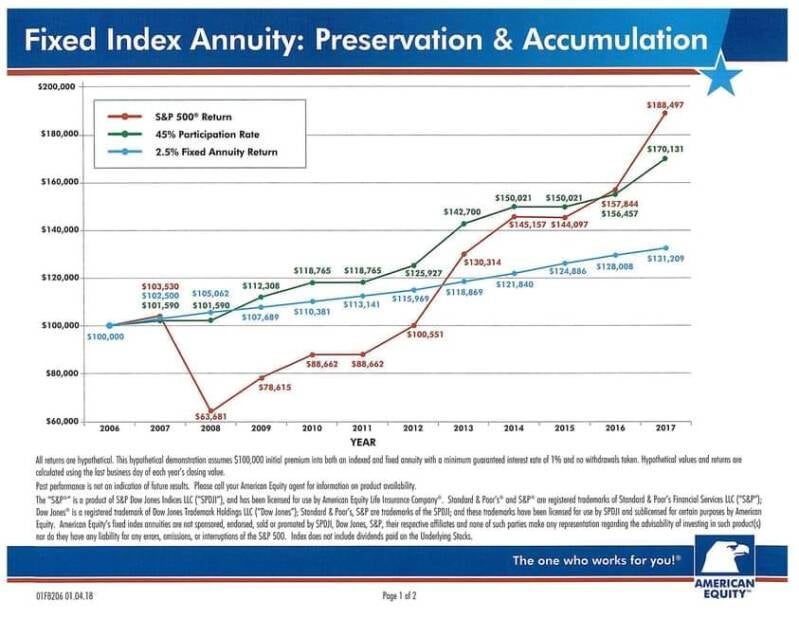

If you are the red line, you are probably going to be where you and a lot of other people were in 2008 real soon. There are ways to protect your funds and ensure you don't lose a single penny of your "nest egg". Regardless of what financial experts on TV might say, there is no investment strategy or financial product that's right for everyone. There can't be, because your financial situation and goals are unique to you.

Without Increasing income, there is no retirement!!! Your retirement security boils down to how much sustainable cash flow your retirement assets can safely and reliably produce. You probably have a valuable home and maybe even a hefty retirement portfolio. Maybe not. However, cash flow may be the most underrated tangible asset you have.

Cash flow is the lifeblood of financial security, happiness, and freedom. Run out of it or have it reduced and your world can be turned upside down. Cash flow, for most, is derived from working. This income allows us to acquire assets. The purpose of those assets (real estate, investments, retirement plans, or interest in a business) is to create an income stream that can eventually replace your paycheck -- which is what we call building wealth. Wealth means the freedom to do things we love and avoid things we don't.

While some think they need to reach a certain "number" to retire, it's really about creating cashflow you can't outlive. It's about how much cash flow you'll have in retirement, not how much you have saved, or even what rate of return you get.

Pensions are uninterrupted, stable, guaranteed income streams but in today's world, not many employers offer them which means not many retirees have them. Without reliable income that keeps up with inflation, you can't have full security in retirement especially with people living longer these days. It is much harder to figure out how to create income for the long haul.

Ask yourself these 5 questions:

- How mush uninterrupted, increasing income can your savings, investments, and retirement accounts generate?

- What could interrupt, reduce, or destroy said income stream?

- What happens when the market goes down? Where will I pull the needed income from while my investment portfolio recovers?

- What happens if tax rates rise to the point that taxes start to reduce your spendable income?

- What happens if the cost-of-living increases at a rate greater than anticipated?

Last but not least, think about how much monthly income you need in retirement and how you are going to generate it. When it comes to retirement, especially in today's inflationary environment, think about how you will protect and create the life you want for yourself in retirement.

Create Your Own Website With Webador